Understanding Oil & Gas Exploration Sector in Pakistan

Introduction

The oil and gas sector in Pakistan, while not as resource-rich as some of its Middle Eastern counterparts, plays a crucial role in the country’s economy. Over the past decade, however, this sector has been grappling with significant challenges, particularly in maintaining production levels. This blog delves into the current state of the industry, analyzes it through Porter’s Five Forces, explores the key challenges faced by exploration and production (E&P) companies, and provides an outlook.

Structure of Pakistan’s Oil and Gas Sector

Pakistan’s oil and gas sector is divided into three main segments: upstream, midstream, and downstream.

Upstream Companies: These are the companies at the top of the supply chain, responsible for extracting oil and gas from the ground. They extract crude oil and natural gas, perform water treatment (since extracted oil often contains water), and sell the crude oil to refineries and the natural gas to distribution companies after treatment.

Refineries: These companies take crude oil from upstream companies and convert it into finished products like petrol, diesel, and kerosene—products used in vehicles and other applications.

Downstream Companies: These companies purchase refined products from refineries and sell them to end-users. Pakistan State Oil (PSO) is a prime example, distributing refined products to consumers through their network of stations.

Currently, Pakistan consumes around 16-17 million metric tons of oil annually. Only 20-25% of this is produced locally; the remaining 75-80% is imported, making Pakistan a significant oil importer. For gas, the country’s consumption stands at approximately 4 billion cubic feet per day, with local production meeting around 80% of the consumption and imported LNG addressing the remaining 20%.

Oil and Gas Sector in Pakistan

Pakistan is not inherently very rich in oil and gas resources. Unlike the Middle Eastern countries, where oil and gas production is abundant, Pakistan’s oil production peaked at approximately 95,000 barrels per day (bpd) in 2015. This increase was driven by major discoveries in the Khyber Pakhtunkhwa (KPK) region, such as the Nashpa and Tal Blocks. However, since 2010, no major discoveries have been made, leading to a gradual decline in production. As of 2024, crude oil production has dropped to around 71,000 bpd.

Similarly, the natural gas sector has faced a decline. Pakistan’s gas production peaked at 4.3 billion cubic feet per day (bcfd) in 2012 but has since fallen to 3.2 bcfd. Major gas fields such as Sui, Uch, and Mari were discovered decades ago, and recent discoveries have been small. This decline in production is a significant concern for the country’s energy security.

Competition and Pricing in the E&P Sector

Given the large gap between demand and supply, companies don’t need to compete aggressively to sell their products — whatever they produce can be sold comfortably. However, this lack of competition doesn’t allow companies to charge any price they want, as the government strictly regulates this sector through pricing policies.

Pricing Factors:

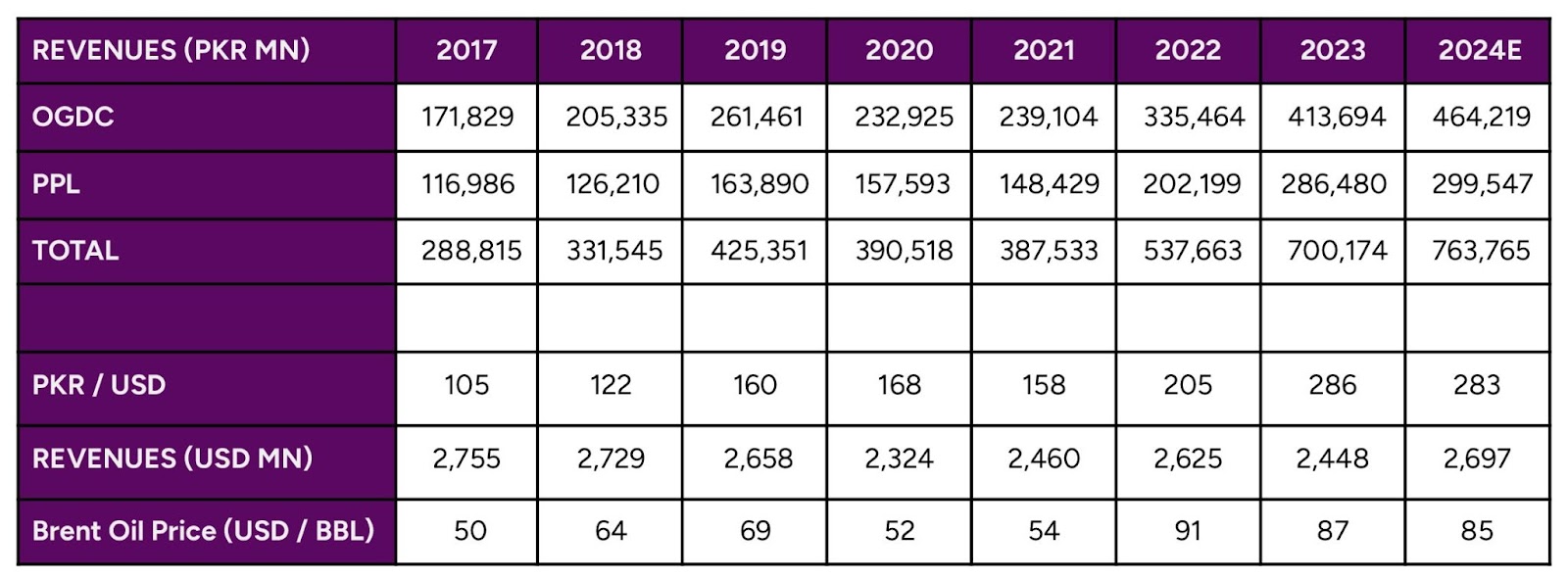

International Oil Prices: The sector’s revenue is linked to international oil prices.

Exchange Rate: Pricing is set in dollars, even though transactions occur in rupees, making the exchange rate a critical determinant of revenue.

Additional Income Sources:

Interest Income: These companies often have significant liquidity, which they invest in government instruments like T-bills and PIBs.

Exchange Gains: Companies also benefit from exchange gains when the local currency devalues.

Key Expenses:

Royalties: Companies must pay royalties to the government, typically ranging between 8-12% of their revenue.

Transportation Costs: This includes the cost of transporting oil and gas from the fields to refineries.

Operating Expenses: These cover salaries, non-cash expenses like depreciation and amortization, and administrative costs.

Exploration Costs: Expenses incurred in conducting surveys and drilling wells that may turn out to be dry.

Porter’s Five Forces Analysis

Porter’s Five Forces is a globally accepted framework to analyze an industry’s structure:

Threat of New Entrants: The barriers to entry in the oil and gas sector are high due to the significant capital investment required for exploration and production. Additionally, the sector is heavily regulated, which further limits the entry of new players.

Bargaining Power of Suppliers: In Pakistan, the government through regulatory bodies defines pricing that can be charged by the E&P companies, limiting the bargaining power of suppliers.

Bargaining Power of Buyers: The government is the single largest buyer of natural gas from E&P companies whereas local refineries buy crude oil. Since pricing is defined through petroleum policies, buyers also have limited bargaining power.

Threat of Substitute Products: The threat of substitutes, such as renewable energy sources, is increasing. However, given Pakistan’s current energy infrastructure, the transition to alternatives like solar and wind energy is gradual. An immediate substitute is imported crude oil, which faces the challenge of limited foreign exchange in the country.

Industry Rivalry: The rivalry among existing players is low since it is a highly regulated sector.

Challenges in the Oil and Gas Sector

The oil and gas sector in Pakistan is currently facing several significant challenges:

Declining Production Levels: As mentioned earlier, Pakistan’s oil and gas production has been on a decline due to the lack of new large discoveries. Maintaining even the current production levels has been a serious challenge.

Increased Exploration Costs: To maintain production levels, companies are forced to increase their exploration efforts, leading to a significant rise in costs. The lack of new discoveries further exacerbates this issue.

Circular Debt Crisis: The circular debt crisis has severely impacted E&P companies in Pakistan. This issue, which emerged around 2008-09, has intensified over the years. The rising receivables and delayed payments have eroded liquidity, forcing companies like Oil and Gas Development Company (OGDC) and Pakistan Petroleum Limited (PPL) to curtail their dividends.

Outlook

In a web of declining production, rising exploration costs, and liquidity constraints, the potential for future growth hinges on following factors:

Exploration Efforts in Abu Dhabi: Pakistani E&P companies have secured offshore leases in Abu Dhabi, a region rich in oil. Success in these endeavors could provide a much-needed boost to the sector.

Resolution of Circular Debt: While there have been efforts to increase gas prices to improve cash flow for E&P companies, more needs to be done.

The oil and gas sector in Pakistan is currently facing several significant challenges:

The oil and gas sector in Pakistan is currently facing several significant challenges: